A Guide to Knowing your Mortgage Numbers

You’ve found your house, you’ve made an offer, buy now you’ve got to decide how to pay for it. With all the options available today, trying to decide on a mortgage can be hard than choosing between cheesecake and apple pie at a Swedish buffet. You’ll get the best deal if you know your options – here’s a guide to the basics of the mortgage selection:

Fixed Rate Mortgages

Looking for stability? Found your dream home and plan to stay there for the next 15 years? Investigate a fixed-rate mortgage. Whether you go with a 15- or 30-year fixed rates, these types of mortgages are like getting an insurance policy on your interest rate – the rate stays the same, so your monthly payment also stays constant. The downside of this most common type of mortgage? While the rates never go up, they also never go down, unless you refinance.

Adjustable Rate Mortgages

Adjustable rate mortgages, or ARMs, have become increasingly popular over the last few years because they start with an attractive, lower fixed-rate, and after an initial period, they adjust according to a specified index. They can look confusing, what with the 3/1, 5/1, 7/1, 10/1 and a handful of other options, but they’re easy to read. The first number indicates how many years your interest rate is fixed; the second number indicates how often the rate adjusts after that initial period is over. For example, in a 5/1 ARM, your interest rate stays the same for the first five years, and then adjusts every year aftermath, up to a cap that you and your lender agree on.

The downfall of these low-rate wonders? After your initial fixed-rate period is over, if interest rates rise, so does your monthly payment. If you can live with that, or if you expect to move in the next few years, then an ARM can save you money over the short term.

Interest-Only Mortgages

Another increasingly popular mortgage option is an interest-only mortgage. This type of mortgage is best for people whose income comes from infrequent commissions or bonuses, or for those who expect to earn a lot of money over the next few years. With interest-only loans, you pay only the interest on your mortgage for a fixed period of time (usually 5 or 7 years). At the end of this period, you can refinance, pay off the mortgage in a lump sum, or start paying off principal (in addition to your interest payments).

Balloon Mortgages

These mortgages are similar to an ARM, in that you get a low initial interest rate, but after a set number of years – usually 5 or 7 – the mortgage ends and you have to either pay off the remainder (with a “balloon” payment, hence the name) or reset the mortgage at current interest rates. Payments are amortized over 30 years at an interest rate that’s typically lower than a fixed-rate mortgage, so if you plan to move before the balloon maturity date you can usually save money. But if you plan on staying put, and interest rates rise dramatically over the next few years, your payments after a reset could increase substantially as well.

Low-Doc/No-Doc Mortgages

If you are self-employed or have bad credit but a lot of cash, a low-doc or no-doc mortgage is a good option. When considering you for a low-doc mortgage, lenders typically look for two of three requirements: assets, income and credit. If you meet two of the three, for the price of slightly higher interest rate you can get easy mortgage approval without having to provide a lengthy financial history.

Sorting out he Acronyms: A Guide to General Mortgage Terms

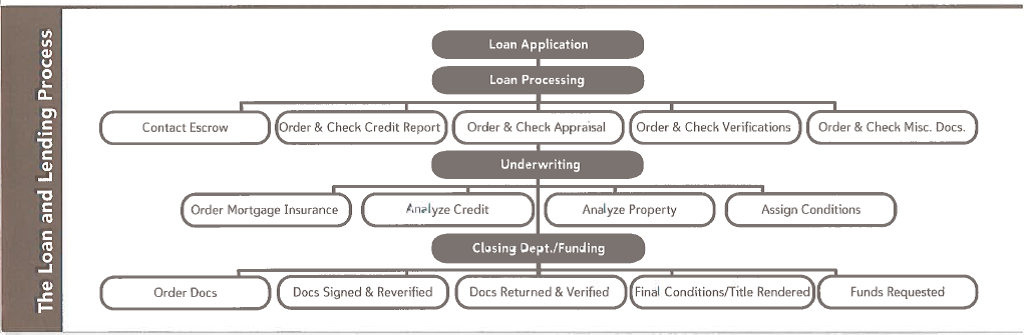

With all the complicated terminology, acronyms and industry lingo used in the mortgage industry, even the expert linguist can sometimes find themselves baffled. Collected below are a few of the more common terms used in lending today. If you feel like you and your lender are speaking different languages, reading the definitions listed below can help you get on the same page. In addition, look to the bottom of the page for a visual map on how the lending process works. Most importantly, when discussing mortgages, make sure you talk to a professional that you can trust.

APR (Annual Percentage Rate)

APR is a number that the Federal government calculates to show the total yearly cost of a mortgage as expressed by the actual rate of interest paid. This number is calculated using a standard formula, which includes the base interest rate, points and any other add-on fees and costs of your mortgage.

Canada Mortgage and House Corporation (CMHC)

Canada Mortgage and House Corporation (CMHC) is Canada’s national housing agency and is Canada’s premier provider of mortgage loan insurance, mortgage-backed securities, housing policy and programs, and housing.

Conventional Loan

A mortgage loan up to a maximum of 75% of the lending value of the property. Typically, the lending value is lesser of the purchase price and market value of the property. Mortgage loan insurance is usualy not required for this type of mortgage (per the CMHC).

GFE (Good Faith Estimate)

Within 72 hours of signing a residential loan application, the federal government requires that a good faith estimate is sent to the borrower, outlining the costs and charges a borrower is likely to incur in connection with the loan closing. However, the GFE is not a guarantee that the applicant will be approved for the loan or that the final amount will be the same figure; the amount (interest rate, terms, conditions) may change pending final loan approval and down payment terms.

MIP (Mortgage Insurance Premium)

The amount that the CMHC charges up front when they insure a loan under one of their programs. The CMHC pays the money into a fund where the money is held until it is needed in the event of a default by a buyer.

PMI (Private Mortgage Insurance)

If a mortgage loan exceeds 80% of the sales price of the home, lenders require insurance coverage that will protect them in the event that a buyer defaults on their loan. The cost of PMI is typically charged to the borrower when the loan to value ratio is greater than 80%.

Points

An upfront cash payment required by the lender as part of the charge for a loan, expressed as a percent of the loan charge equal to 3% of the loan balance.

Preapproved

A general term that means that a borrower has completed a loan application and provided their debt, income and saving information which an underwriter has reviewed and approved.

Prequalification

A preliminary step in the loan application process, a prequalification is a lender’s written opinion of the ability of a borrower to qualify for a particular loan amount. The amount prequalified by the lender is determined based on inquiries into the borrower’s debt, income and savings, and may or may not require a credit check.

Ratios

Ratios are used in the lending industry to determine the probability of a borrower being able to repay a loan – usually this ratio compares the borrower’s fixed monthly expenses to his gross monthly income. Certain lenders have different ratio requirements; for example, the CMHC requires that a monthly mortgage payment is no more 32% of monthly gross income (before taxes), and that the total of mortgage payment and non-housing debts is less than 40% of income.

In lending these two figures are represented as 32/40: 32 is the Gross Debt Service (GDS) Ratio (gross monthly income divided by monthly mortgage principal and interest, taxes and heating expenses); 40 is the Total Debt Service (TDS) Ratio (gross monthly income before taxes divided by monthly mortgage payment plus non-housing debts, such as car loans and credit card debt).

TLS (Truth in Lending Statement)/Regulation 2

A federal law that requires lenders to fully disclose, in writing, the fees, terms and conditions associated with the loan, including annual percentage rate (APR) and other charges.

VA (Veterans Affairs)

The department of the federal government that handles all programs associated with veterans of the Canadian military; in the mortgage industry, the agency guarantees loans that are made to veterans (similar to mortgage insurance), thereby encouraging lenders to make mortgages to veterans.

For more information on how I can help you get into your dream home, do not hesitate to contact me, Leslie McDonnell, RE/MAX Select Properties 778-838-2378.